iConnectHub

iConnectHub

Login/Register

Login/Register Supplier Login

Supplier Login

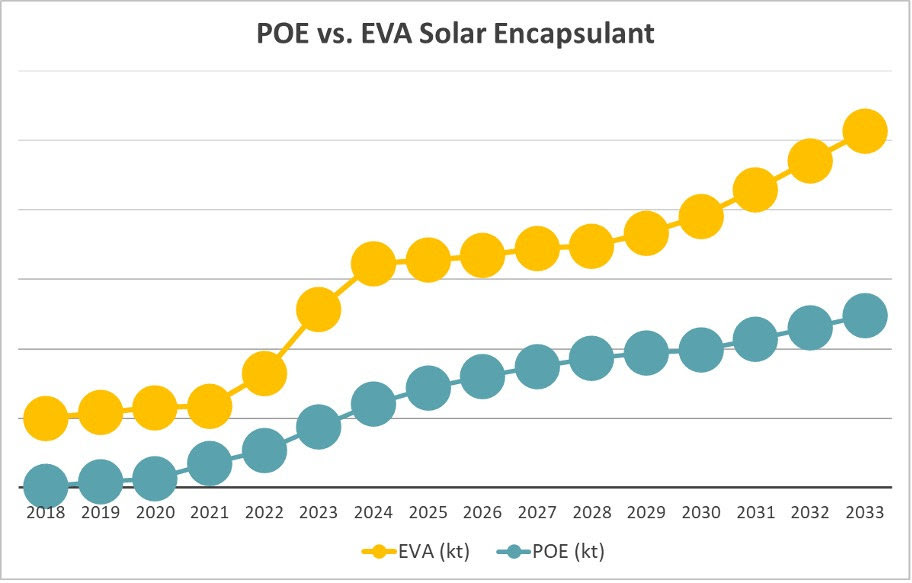

The global market for polyolefin elastomers and plastomers (POEs/POPs) is forecast to grow at 6.3% per annum (CAGR) through to 2033 to a volume of 3.8 million tonnes-plus according to the latest iteration of MLT Analytics’ Global Ethylene-based POE/POP Report—A Detailed Market and Technology Overview (2022–2033) released recently. This impressive growth is being fueled largely by strong gains in solar module encapsulation film as deployment of utility-scale solar farms and residential solar panels continues to exceed expectations and supported by solid growth in impact modification of automotive polypropylene (PP) compounds.

“The solar module industry is experiencing an era of dynamic transformation, with module makers promoting competing cell structures such as TOPCon and HJT, each of which have their optimal encapsulation structures,” says MLT Analytics CEO and co-founder Stephen Moore. “In many cases, the encapsulant solution may employ a combination of POE and EVA resins. We anticipate strong consumption growth for both resins, with the exact resin mix depending on which cell technology emerges as the dominant force,” he adds.

In the automotive sector, POE continues to be a material of choice for impact modification and while unit production of vehicles is stagnant and even forecast to decline in some developed markets, growth potential remains due to increased use of PP compounds as a lightweighting lever in electric vehicles (EVs) in particular. “An additional growth factor in Europe is impending EU legislation requiring certain levels of plastics recovered from end-of-life (EOL) vehicles to be recycled and reused in new vehicles, which may be mandated from 2030 onwards,” says Moore. “Lower quality base resins on account of their recycled content will require higher levels of compatibilization and impact modification to ensure that PP compounds meet OEM performance standards, and POEs are the natural enabler,” he explains.

Sealant film is viewed as a promising market for POPs, particularly considering the trend towards increased adoption of monomaterial, multilayer flexible packaging structures but with one major one caveat. Suppliers of metallocene-catalyzed LLDPE are marketing sealant film grades with POP-like densities that incorporate less hexene or octene comonomer compared to POPs. “Such materials have a cost advantage versus pure POPs and often, their sealing properties are more than sufficient for the application at hand,” says Moore.

On the supply side, incumbent POE/POP suppliers from North America, Europe, Japan and South Korea will soon no longer have the market to themselves. To an extent in line with China’s national policy to localize supply of key components in high tech sectors including green energy, 2024 and beyond will see the emergence of multiple new suppliers of POE in China. “We count 20 potential new Chinese POE players in our latest supplier database,” notes Moore. “And while there’s no guarantee that all projects will go ahead, nor is there any certainty that those projects that do materialize will be able to produce commercially viable POE grades in the short to medium term, or indeed ever, we do expect several new suppliers to succeed and transform the supply situation in the process.”